Eton Solutions Alternatives for Single- and Multi-Family Offices

Top Alternatives to Eton Solutions Start With Where Eton Fits and Where It Doesn't

The search for top alternatives to Eton Solutions becomes clearer once the question shifts from brand gravity to operating fit. Eton Solutions is best understood as a platform built for environments where reporting, accounting, and office operations need to stay coordinated instead of living in separate systems. That makes the real comparison less about feature volume and more about whether the platform matches the office's structural demands.

- Use Eton as the benchmark when shared reporting and accounting control matter across multiple entities and workflows.

- Look elsewhere when the platform-weight and process discipline outpace what a lean office actually needs.

- Carry that fit vs mismatch lens into the next section, where the buying dimensions do the separating work.

Where Eton Solutions Stands out in Reporting, Accounting, and Family Office Operations

The strongest case for Eton Solutions appears when complexity is already structural. In that setting, the value is not a longer list of solutions. It is a shared control layer that keeps reporting, accounting, and operational processes aligned across complex structures, multiple entities, and family office responsibilities that cannot be managed cleanly in isolated tools.

- Reporting stays tied to the same operating environment as accounting, which matters when oversight depends on one version of the record.

- Accounting depth sits closer to day-to-day office work, including bill pay and administrative coordination, rather than standing apart as a separate back-office function.

- The platform fit strengthens when a family office needs one system to support visibility across ownership layers, workflows, and recurring operating controls.

That is the benchmark the rest of the comparison should use. The issue is not software breadth on its own. It is whether reporting, accounting, and operations truly need one control layer.

Why Some Family Offices Still Need an Alternative

A strong benchmark can still be the wrong fit. Some family offices do not need a platform designed around broad operating control, and the mismatch usually appears when enterprise-style process expectations create more structure than the office needs. For a lean team, that can mean extra platform weight, more workflow discipline, and added accounting overhead before the office gains meaningful decision value.

- Lean family offices may want simpler oversight and cleaner reporting without adopting a heavier operating model.

- Other family offices may need deeper accounting control than a general family-office platform emphasizes, especially when entity complexity drives the search.

- RIAs and multi-asset teams may need a platform with broader client-service, portfolio, and succession planning workflows than a family-office-centered system is built to prioritize.

So the alternative search should not ask which platform looks bigger. It should ask which buying dimensions reveal the right fit.

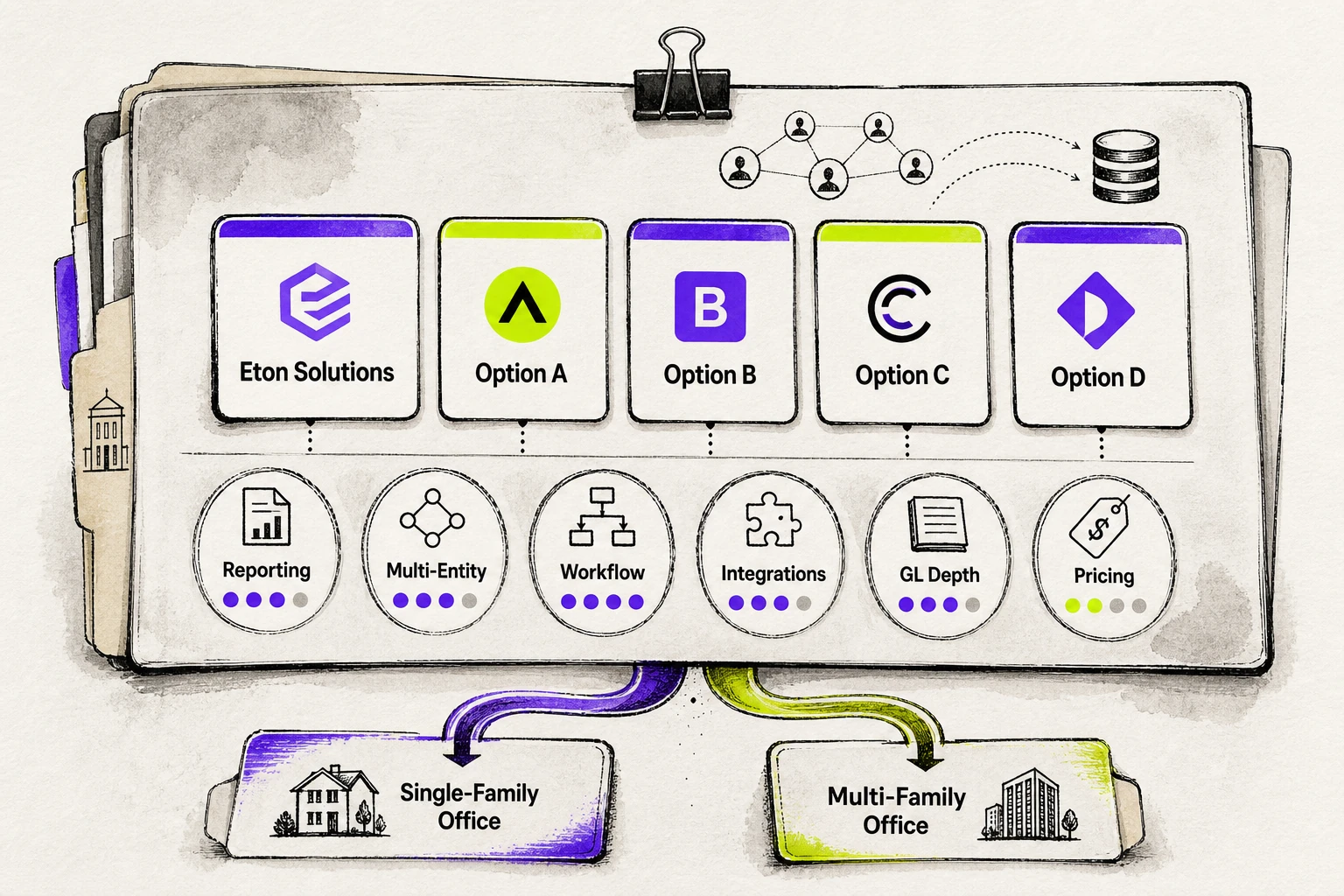

Which Buying Dimensions Actually Separate Eton From the Field

The real separation in this market comes from five operating questions: multi-entity control, workflow coverage beyond reporting, whether data is truly shared across the platform, how much accounting depth the office needs, and how much buyer risk sits inside pricing opacity and total cost of ownership. The table stays narrow on public pricing signals and avoids false precision across other platforms.

| Dimension | Eton Solutions | Addepar | Allvue Systems | FundCount |

|---|---|---|---|---|

| Pricing transparency | Mixed. EtonAlpha publishes a product-specific annual fee range; broader enterprise pricing stays sales-led. | Contact-led in official material reviewed. | Contact-led in official material reviewed. | More transparent in official material reviewed, with a starting-from asset-management price and pricing-model context. |

| Implementation-cost transparency | No fixed public implementation amount verified. | No fixed public implementation amount verified. | No fixed public implementation amount verified. | Implementation is described as scoped or phased, but no fixed public implementation amount verified. |

| Safe editorial takeaway | Do not generalize EtonAlpha pricing to every Eton offering. | Treat pricing as custom in the reviewed market material. | Treat pricing as custom in the reviewed market material. | Keep any number tied to its product segment and access date. |

That framework gives later vendor comparisons a shared reporting, accounting, and cost standard.

How Reporting Consolidation and Multi-Entity Control Affect Oversight and Complexity

Oversight breaks first at the reporting layer. Once an office is tracking multiple entities, liquid and illiquid assets, several asset classes, and multi-currency exposure, the problem is no longer producing reports. It is producing a consolidated view that can still be trusted when ownership, cash movement, and valuation records cut across structures. That is where multi-entity control starts to matter.

A lighter office can often tolerate more manual stitching. A more complex office cannot, because reporting efficiency falls as soon as separate records must be reconciled across multiple entities and different data sources. The requirement is structural: clean reporting depends on whether the system can hold complexity without pushing control back into spreadsheets, side calculations, or disconnected teams.

Custodian Integrations and Workflow Coverage in One Platform

Connectivity is only part of the buying test. A platform may handle data integration and data aggregation well, yet still leave core office work outside one platform, which forces repetitive tasks back onto staff and weakens operational efficiency. The better comparison is qualitative: does the system stop at aggregation and reporting, or does the platform also support the workflows that turn incoming data into controlled action?

- Test whether connected data can move into actual workflow coverage, such as review, approval, exception handling, or follow-up steps, rather than ending at a dashboard.

- Ask where intelligent document processing or intelligent automation reduces repetitive tasks and where staff still need manual handoffs.

- Check whether users can act inside one platform or whether key tasks still depend on exports, email chains, or separate tools.

- Treat custodian connectivity and workflow breadth as one decision, because aggregation alone does not create operational control.

How Fully Integrated the Platform Really Is

A common interface does not make a platform fully integrated. The stricter test is whether financial data, approvals, and operational records run through unified data in a centralized hub, or whether the system is still coordinating multiple disconnected tools behind the screen. That distinction matters because a fully integrated design can improve data management and reduce reconciliation, while a looser stack may preserve more choice for teams that prefer separate systems or financial institutions.

- Look for a single source of truth rather than separate modules that only share a visual layer.

- Check whether changes in one area update related financial data elsewhere without manual re-entry.

- Ask how the platform handles real time data versus delayed synchronization across tools.

- Treat unified data and shared controls as the proof of a fully integrated platform, not a sales claim.

How General Ledger Depth Changes Accounting Burden and Operational Fit

General ledger depth becomes decisive when portfolio accounting stops being enough. If the office must manage multiple ownership layers, entity-level obligations, journal entries, and reporting that cannot be handled safely in side spreadsheets or parallel accounting tools, a deeper general ledger can justify the added administrative load and reduce manual work. If those requirements are light, extra accounting structure may add more burden than value. Choose more ledger depth when control requirements are expanding faster than portfolio accounting can absorb them.

What to Watch for in Pricing Transparency and Total Cost of Ownership

Headline pricing rarely captures the real buying risk. In the official material reviewed, EtonAlpha shows a product-specific annual fee range of $25K to $125K, FundCount shows asset-management pricing from $35,899 per year, and its FAQ separately notes an average entry license fee of about $25,000 USD. Other reviewed platform pricing remains contact-led, and none of the reviewed official pages publish fixed implementation-cost amounts.

- Keep product-specific figures separate. EtonAlpha pricing is not enterprise Eton pricing, and FundCount's starting-from asset-management figure is not the same as its average entry license note.

- Assume onboarding effort matters. Data cleanup, process redesign, and administrator time can change total cost of ownership as much as the platform fee.

- Treat contact-led pricing as buyer risk, because operating scope may stay unclear until the sales process defines it.

- Ask for implementation assumptions in writing, even when no fixed public amount exists.

The Right Alternative Depends on Your Office Model and Decision-Making Needs

Software fit changes with the operating model. The same platform can feel right for one office and heavy for another because reporting, family office services, internal coordination, and decision making do not scale the same way across teams. In practice, the question is not whether one platform handles more services. It is whether that platform matches the records, workflows, and control points the office actually needs in one platform.

- Lean single-family offices usually need clean reporting and core oversight without enterprise-level weight.

- Multi-family offices feel workflow strain sooner because service breadth, shared processes, and cross-team coordination expand together.

- RIAs and multi-asset managers often judge fit through broader client, portfolio, and service workflows rather than family office administration alone.

Lean Single-Family Offices That Need Less Complexity

Overbuying is often the first mistake. When family offices have a limited entity structure, a smaller internal team, and straightforward reporting needs, a heavier platform can add operating burden before it adds control. The issue is not software quality. It is a mismatch between system weight and the actual coordination problem.

- A lean single-family office usually values faster adoption, clearer reporting, and less administrative overhead.

- The platform fit improves when the office does not need deep cross-entity process controls or broad service workflows.

- In this scenario, family offices often benefit more from simpler oversight than from enterprise-level process depth.

Multi-Family Offices That Need More Operational Depth and Fewer Workflow Gaps

Breadth changes the requirement. As family offices serve more relationships, more staff, and more service lines, workflow gaps start to create operating risk because reporting requirements, reviews, approvals, and follow-up tasks no longer stay contained inside one team. What looked manageable in a lean model becomes harder to control across a multi family office structure.

- This model needs stronger operational depth because family offices must align data, processes, and service delivery across multiple relationships.

- The cost of fragmented reporting rises when staff members depend on the same records but work through different handoffs.

- Fit improves when the platform reduces workflow gaps rather than leaving teams to patch services together manually.

This branch should pay closer attention to alternatives built for wider coordination, deeper oversight, or both.

RIAs and Multi-Asset Managers That Need Broader Client and Portfolio Workflows

The center of gravity shifts again in advisor and manager models. Financial advisors, wealth management firms, and asset managers often need the platform to support relationship coverage, portfolio oversight, and recurring service activity across many clients, not just the internal administration of a family office. That changes the buying logic because the client-servicing model becomes as important as accounting depth.

- RIAs and multi asset managers usually value broader client workflows, portfolio processes, and service coordination.

- Wealth management priorities can differ from family-office priorities when the team serves many households or mandates at once.

- For asset managers, the better path is often the branch that emphasizes broader workflow coverage before deeper family-office administration.

The next step is to follow the branch that matches the office model first, then compare the named alternatives inside that path.

Best Alternatives if You Want a Simpler Platform Than Eton

A simpler platform can be the better choice when the office does not need maximum accounting breadth or the heaviest operating model. In this branch, the comparison is about what each option reduces by design: Addepar leans toward reporting and analysis, AssetVantage sits in the middle with family office coverage without the same enterprise weight, and Archway can appeal to teams that want meaningful capability without the broadest scope. Masttro also sits in this landscape as a reporting- and analysis-oriented platform, but the sharper fit distinctions here center on the three options below.

| Vendor | Best for | How it differs from Eton Solutions | What the lighter fit means |

|---|---|---|---|

| Addepar | Teams prioritizing performance reporting and portfolio analysis | More reporting-centered than one system for accounting and daily administration | A stronger fit when analysis matters more than broad operating coverage |

| AssetVantage | Teams that want a middle ground between basic reporting tools and heavier family-office systems | Family office coverage without enterprise weight | A lighter operating footprint that can suit leaner teams |

| Archway | Teams wanting substantial family-office capability without the broadest possible platform scope | Preserves meaningful family-office capability without Eton-level breadth | A narrower scope can be an advantage when maximum unification is unnecessary |

| Masttro | Teams looking at the reporting and analysis landscape | More centered on wealth data visibility than on broad accounting or office operations | Useful as a lighter comparison point, even if the tighter fit distinctions here sit elsewhere |

The issue is not less software; it is tighter scope aligned to a leaner operating requirement.

Why Addepar Fits Teams That Prioritize Reporting Flexibility Over All-in-One Operations

Addepar fits best when the office values reporting flexibility more than unified daily administration. The trade-off is structural: it is positioned more around performance reporting, portfolio analysis, and visibility across investments than around serving as one operating system for accounting and wider family office coordination. For a lean team that mainly needs clearer analysis, support for private investments, and real time insights for oversight, that narrower center of gravity can be an advantage rather than a gap.

- Best Fit: teams where reporting, portfolio analysis, and performance reporting matter more than broad office operations.

- Why It Can Feel Lighter: the platform is more reporting centered, so buyers are not selecting it primarily for unified accounting and daily administration.

- Practical Trade-off: if the office wants one platform to carry a wider operating burden, the fit may weaken even if the reporting remains strong.

AssetVantage if You Need Family Office Coverage Without Enterprise Weight

AssetVantage sits in the middle ground. It can suit a family office that wants broader reporting and accounting coverage than a pure analysis tool, but does not want the same enterprise weight as a larger platform choice. That makes it a practical alternative investment for leaner teams that still need operating visibility across the office. The appeal is balance, not maximum scope.

- Best Fit: teams that want family-office coverage without committing to the heaviest operating model.

- Why It Can Work: lighter-weight can be easier for smaller teams to absorb while still supporting reporting and accounting needs.

- Practical Limit: as entity count, process complexity, or oversight demands rise, a lighter structure may become less ideal.

Archway if You Want Family Office Capability Without Eton-Level Platform Breadth

Archway fits buyers who still want substantial family office capability, but do not want the broadest possible platform scope. In this branch, the appeal is not minimalism. It is a tighter focus on meaningful reporting and accounting needs without assuming that maximum operational unification is the goal. For some offices, that narrower focus creates a cleaner fit than adopting a wider system than the model requires.

- Best Fit: offices that want meaningful family-office capability with a more selective focus.

- Why the Narrower Scope Can Help: less breadth may be a feature when the office wants stronger focus without the widest platform footprint.

- What This Sets up Next: if the real requirement is deeper accounting control rather than lighter-weight, the comparison changes.

Best Alternatives if You Need More Accounting or Multi-Entity Depth

Some alternatives earn consideration because the real risk is not missing a lighter interface. It is losing control as reporting and accounting spread across layered entities, ownership rules, and ledger demands. In this branch, Archway Platform is the clearest evidence-backed fit when partnership accounting and multi-entity depth drive the search. FundCount is a qualitative alternative when continuous accounting and general-ledger discipline matter as much as investment visibility, while Allvue sits more naturally in the landscape for private-capital managers than for family-office-operating alignment. The distinction is structural: this path favors accounting control over lighter workflow breadth.

SEI Archway Platform When Partnership Accounting Drives the Search

Archway Platform fits the buyer case where ownership logic drives the software decision. When a family office or investment structure has layered entities, private equity style capital activity, and specialized cash flows that must stay tied to the books, the issue stops being dashboard breadth and becomes accounting architecture. Archway Platform is positioned as a ledger-centric platform built as one system with one general ledger serving as both the investment book of record and the accounting book of record. That matters when oversight depends on keeping investment activity, entity records, and accounting control aligned inside the same operating structure.

- Partnership accounting is the central fit case. Archway Platform supports waterfall calculations that can be posted as journal entries derived from fund agreements.

- Its one-ledger architecture is built for conditions where the same platform must support investment records and accounting records without forcing a handoff between disconnected systems.

- The platform is designed to handle complex, multilayered entity hierarchies, including fund-of-funds structures that increase ownership and allocation complexity.

- Accounting workflows extend beyond close reporting. The platform includes invoice intake, approval routing, payment creation, reconciliation, and automated accounting workflows on the same platform.

- The strongest fit appears when partnership accounting, entity complexity, and accounting precision matter more than broader adviser workflow coverage or a lighter operating model.

Historically, SEI materials tied the platform to family-office and private-fund use cases, which reinforces the same pattern: Archway Platform becomes more compelling as partnership accounting, ownership structure, and entity-level control become the buying center. The issue is not feature volume; it is whether the operating model needs one-ledger discipline.

FundCount if General Ledger Control Matters as Much as Investment Reporting

FundCount fits a different version of the same control-heavy search. The buyer is still prioritizing accounting, but the center of gravity moves from partnership-accounting specialization toward general ledger discipline and continuous accounting. In that frame, FundCount becomes attractive for firms that want investment reporting tied closely to a real time general ledger rather than treated as a separate layer. The appeal is not broader client-service workflow. It is tighter ledger control when accounting precision has to keep pace with ongoing activity.

- The best fit is the environment where fund accounting and general ledger control matter as much as investment visibility.

- The Trade-off Against Eton Is Qualitative but Clear: the orientation leans more heavily toward continuous accounting and ledger discipline.

- This can suit operating models that want accounting oversight kept closer to ongoing investment activity and reporting.

- Firms working closely with fund administrators may prefer this posture when the accounting record needs to stay central to day-to-day control.

- Compared with Archway Platform, the distinction is emphasis rather than a verified feature hierarchy: FundCount points the reader toward ledger rigor, while Archway Platform is the stronger evidence-backed option for partnership-accounting and multi-entity depth in this category.

Allvue merits brief note only as another qualitative option in the accounting-depth landscape for alternative investment managers in private capital markets. The next decision path is different: some teams do not need deeper accounting at all, but broader client-service and advisor workflows instead.

Best Alternatives for Multi-Family Offices, RIAs, and Multi-Asset Managers That Need Broader Client-Service Workflows

| Vendor | Best fit | How it differs from Eton |

|---|---|---|

| Addepar | Cross-relationship reporting and portfolio oversight across multiple relationships | More reporting-centered than a system chosen for accounting and daily family-office administration |

| Black Diamond | Wealth management workflow around the portfolio in relationship-driven service models | Better aligned to relationship-driven service workflows than to deeper multi-entity accounting and family-office operations |

| Tamarac | Rebalancing, trading, and advisor operations for execution-heavy service models | More pointed at execution-heavy advisor workflows than integrated family-office accounting and ownership oversight |

| Advisor360° | An additional option in the broader wealth-management productivity landscape | Positioned as a broader productivity option rather than a family-office-centered operating platform |

Control is not the only buying lens. Once family offices, asset managers, or advisory teams serve many clients and relationships at scale, the decision shifts from family-office operating alignment toward broader client-service workflows, communication, and execution support. In that branch, Addepar fits firms that center reporting and cross-relationship oversight, Black Diamond fits service models built around portfolio-facing wealth-management workflow, and Tamarac fits teams where rebalancing and advisor operations matter more than ownership oversight. Advisor360° also sits in this wider landscape as an additional wealth-management productivity option. The governing distinction is simple: some platforms are built to coordinate family offices, while others fit firms that organize work around reporting, clients, and portfolio service breadth.

Addepar if You Need Client Reporting and Portfolio Oversight Across Multiple Relationships

Addepar fits this branch for a different reason than it does in the simpler-platform discussion. Here, the value is not in reduced complexity by itself. The stronger fit is scalable reporting and portfolio oversight across many client relationships, especially when a firm needs one platform to help interpret investments across households, entities, or reporting groups without making family-office administration the center of the buying decision. That matters for firms managing investments across relationship-heavy service models where portfolio performance has to be communicated clearly across varied stakeholders, including private banks and institutional investors, even if the core fit is broader than either label alone.

- Best Fit: teams managing investments across multiple client relationships and needing reporting that scales across those relationships.

- Why It Can Work: the platform is better aligned to investor portals, oversight views, and communication around investments than to embedded accounting-heavy administration.

- Main Trade-off Versus Eton: the fit is more reporting centered than a platform chosen to unify accounting and day-to-day family-office operations.

- Use This Branch When: the operating question is how to present and oversee portfolio performance across clients, not how to run deeper ownership and accounting control inside one family-office structure.

Black Diamond if You Need Wealth Management Workflow Around the Portfolio

Black Diamond belongs in this cluster when the operating center is the client relationship rather than the family-office entity stack. The appeal is wealth management workflow around the portfolio, which makes it easier to evaluate for wealth managers serving many households and accounts where client data, service coordination, and day-to-day portfolio communication shape the platform choice. In that model, the software is less about deep family-office accounting and more about supporting the surrounding service process that wealth management professionals run every day.

- Best Fit: firms that organize work around portfolio-facing service, advisor coordination, and ongoing relationship management.

- Why It Can Work: the platform is better aligned to wealth management workflow than to a family-office structure built around multi-entity accounting depth.

- Main Trade-off Versus Eton: the fit is stronger for relationship-driven service models than for operating environments that need deeper ownership, entity, and accounting control.

- Use This Branch When: the main requirement is keeping wealth managers and client-facing teams aligned around the portfolio, rather than centering the platform on family-office administration.

Tamarac if You Need Rebalancing, Trading, and Advisor Operations Beyond Family Office Reporting

Tamarac is the clearest fit in this branch when execution drives the platform search. Some firms do not need software mainly to coordinate family-office records. They need portfolio management support tied to rebalancing and trading operations, plus advisor workflows that keep ongoing service moving across many relationships. In that context, reporting still matters, but it supports an execution-heavy operating model rather than acting as the front end of a broader family-office accounting structure.

- Best Fit: advisory businesses where rebalancing and trading operations sit close to the center of daily work.

- Why It Can Work: the platform is oriented to advisor operations and portfolio management tasks that follow active execution needs.

- Main Trade-off Versus Eton: the fit is stronger for execution-heavy service models than for integrated ownership oversight or deeper accounting control.

- Use This Branch When: the platform has to support portfolio decisions in motion, not just consolidate reporting for a family office.

That distinction should shape the shortlist. Once the execution model, client-service breadth, and accounting expectations are clear, the vendor list usually gets smaller on its own.

How to Turn the Comparison Into a Practical Shortlist

The right shortlist starts by removing a mismatch, not by forcing every option into one rank order. First, sort by complexity: if the office runs with limited entities and lighter coordination, remove platforms built for heavier operating depth. Next, test accounting: if deeper control is central, keep only options that can carry that burden. Then check the client-servicing model: the platform should match whether the office serves one family, many relationships, or a broader advisory structure.

Choose Based on Complexity, Accounting Depth, and Client-Servicing Model

Three filters usually narrow the field faster than feature-by-feature comparison. Start with the operating model, then test how much entity complexity the team manages, how much accounting control it needs, and whether the office serves one family, many relationships, or a broader advisory book. That sequence turns a broad platform search into a cluster-based matrix.

| Operating profile | Complexity level | Accounting depth needed | Client-servicing model | Likely fit cluster |

|---|---|---|---|---|

| Lean office with limited entities and lighter operational layering | Lower | Basic to moderate | Primarily one family or a narrow internal team | Simpler reporting-first platform |

| Office with multiple entities, ownership layers, and tighter internal controls | Higher | Deeper accounting and multi-entity oversight | Single-family or multi-family office with more operational depth | Family-office platform with stronger accounting structure |

| Organization serving many client relationships with portfolio oversight and service workflows | Moderate to high | Moderate accounting, with broader workflow coverage | RIA, multi-family office, or multi-asset manager | Broader client-workflow platform |

If two clusters still look plausible, use the harder test. Ask which operating burden creates the most risk today: entity complexity, accounting control, or service-model sprawl. The best shortlist is the one that aligns the platform to the office model before the demo process turns into a feature debate.

The Non-Negotiables That Lead to a Better-Fit Vendor Shortlist

A shortlist improves when early screens remove options that cannot support the operating model. These non-negotiables test whether the system can carry the office without adding hidden coordination work.

- Confirm entity complexity fit. The system should match the number of entities, ownership layers, and reporting structures the office already manages or expects to add.

- Verify accounting control. If the office depends on deeper accounting, the shortlist should reflect that requirement before interface preferences enter the discussion.

- Test integration coverage. Custodians, portfolio records, and connected data flows should support oversight without repeated manual reconciliation.

- Check workflow fit. The platform should support the real service model, whether that means family-office coordination, multi-client servicing, or broader advisor operations.

- Pressure-test implementation burden. A strong fit on paper can still fail if the team cannot absorb setup, data cleanup, governance work, and change management.

Use these screens before full evaluations. Better vendor selection comes from eliminating structural mismatch early, then taking a small, fit-based list into demos and due diligence.