Compare Landytech Alternatives by Pricing, Reporting, and Fit

What are the top alternatives to Landytech?

The article ranks FundCount, Addepar, Asora, Dynamo, and Copia Wealth Studios as the top Landytech alternatives by firm fit. In the weighted comparison, FundCount scores 4.65, Addepar 4.63, Asora 3.53, Dynamo 3.44, and Copia Wealth Studios 3.21, with fit depending on reporting, consolidation, data aggregation, and controls priorities.

Why Firms Replace Landytech Before They Shortlist Alternatives

Replacement searches usually start when the platform no longer fits the firm’s operating shape. As firms add entities, asset types, and more stakeholder-ready output, pressure builds in the places that matter most: reporting, consolidation, and day-to-day workflow. That is a structural mismatch. In plain terms, the system may still work, but it no longer supports how the firm actually needs to run.

The early warning sign is often reporting strain. Teams can produce reports, but the process becomes slower, more fragile, or harder to tailor for different audiences. Reporting challenges rarely stay isolated for long because they usually expose a deeper model problem: data is hard to combine cleanly, views are harder to customize, and each new request adds more operational drag.

- Weak consolidation shows up when growth adds accounts, entities, or asset complexity faster than the platform can unify them into a clear view.

- Workflow breakage appears when teams rely on extra steps, side files, or repeated handoffs just to keep reporting and oversight moving.

- Migration risk is not only about moving data. Reporting continuity also matters because a new platform has to preserve dependable outputs when the old and new data models differ.

Once the problem is defined this way, the comparison gets sharper. The next step is to use criteria that reveal structural mismatch quickly instead of relying on surface-level brand impressions.

The Criteria That Separate Similar-Looking Platforms

Once the replacement problem is clear, the next mistake is comparing platforms by surface similarity. Similar demos can hide very different operating models, so the safer approach is a fixed evaluation rubric that tests how each option handles books and records, reporting output, consolidation, data inputs, access control, and adoption effort.

That rubric is meant to frame the later scored comparison, not replace it with another scorecard here. Treat each criterion as an evaluation question rather than a verdict: what must the platform do for this firm, where would weak depth create friction, and which tradeoff matters most before any shortlist is trusted?

Accounting & General-Ledger Depth

Accounting depth separates a reporting layer from a platform that can support finance operations. Buyers should test whether the system only displays balances and transactions or can support a real book of record with ledger structure, reconciliation logic, entity-level treatment, and workable controls.

- Check whether the ledger structure can reflect entities, accounts, and currencies instead of a flat reporting view.

- Ask how reconciliations are handled when positions, cash activity, or entity records do not line up, because shallow support usually breaks there first.

- Verify whether finance teams can trace changes to underlying records and maintain controls around adjustments.

The practical question is whether the platform helps produce trusted numbers or mostly repackages numbers produced elsewhere.

Reporting & Dashboard Flexibility

Reporting flexibility matters when the same data has to answer different stakeholder questions. For family offices reviewing the top alternatives to Landytech, the test is whether family office reporting can give different audiences useful investment reporting, consolidated reporting, and performance reporting without forcing every request back into a static template. In plain terms, buyers should ask whether customizable reporting makes report production easier when portfolio performance needs more than one view.

- Check whether dashboards can be adapted for principals, operations staff, and advisers without rebuilding the whole view each time.

- Treat fixed layouts as a warning sign if reporting flexibility is central, because polished templates alone do not equal adaptable output.

Multi-Entity & Consolidation

Multi-entity consolidation becomes decisive when the firm does not operate as one clean portfolio. Buyers with complex ownership structures should test whether the platform can handle data consolidation across entities, accounts, and reporting views without forcing teams to patch together spreadsheets before producing consolidated reporting. That is not just a reporting preference. It is an early signal of whether the system fits the structure of the business.

- Verify whether multi entity consolidation works across legal entities, vehicles, and household-level views rather than inside a single reporting layer.

- Check how the platform treats eliminations, rollups, and exceptions when one structure needs several views of the same underlying holdings.

- Ask where teams still need off-platform workarounds, because that is usually where structural complexity will resurface later.

Data Aggregation & Custodian Feeds

Data aggregation shapes how current and trustworthy the reporting can be. A platform may look strong in the interface, but weak investment data aggregation can still slow reviews and weaken confidence if automated data aggregation from key data sources arrives late, inconsistently, or in formats that need extra cleanup. Buyers should evaluate data aggregation as an input-quality issue, not just an integration checklist.

- Test whether investment data from different custodians and sources can be normalized into one usable view.

- Ask how the platform handles exceptions, stale feeds, and missing records before they affect client or internal outputs.

- Treat broad connection claims cautiously if the team still needs significant intervention to make the data aggregation usable.

Security & Permissioning

Capability alone is not enough if the wrong people can see or change the wrong records. Security and permissioning should be tested as operating controls: who can access sensitive financial information, how user permissions can be limited by role, entity, or function, and how the platform supports data protection without slowing routine work. That is where data security becomes a fit question rather than a background IT concern.

- Check whether user permissions are precise enough for executives, operations staff, investment teams, and outside advisers.

- Look for controls that support data protection across reports, dashboards, and underlying records, not only at the account level.

- Ask how the team would detect threats or unusual access before an error or exposure reaches a stakeholder.

Usability & Onboarding

Usability and onboarding complete the rubric because feature depth only matters if teams can adopt it. Some firms can absorb more setup, while lean teams may value a faster path to operational efficiency even if that means narrower flexibility in a few areas.

- Check how much configuration, training, and process cleanup must happen before the first usable output is available.

- Ask whether common tasks are clear for everyday users on day one or whether the platform depends on a small expert group.

- Treat long rollout effort as manageable only when the added complexity clearly supports the firm's structure, controls, or reporting needs.

The core question is how much complexity the organization can realistically carry before the tool becomes harder to use than the process it is meant to improve.

Which Landytech Alternatives Fit Family Offices, SFOs, and Other Firm Types Best

The rubric does not carry the same weight for every buyer. Family offices often care most about flexible presentation, wealth management visibility, and how cleanly a platform serves family members, while multi family offices, a single family office, wealth managers, and financial advisors may put more weight on control, scale, or consolidation.

That firm-fit lens narrows the field before the ranked comparison appears. The shortlist becomes more useful when each buyer-context sets the criteria first, so the later table reads as a buyer-context comparison rather than a generic feature list.

Family Offices That Need Flexible Reporting From Family Office Software

For a reporting-led family office, presentation quality shapes how clearly the team explains holdings and performance across family members, especially when multi generational wealth creates different expectations.

| If this describes the firm | Weight these criteria most | Why it changes fit |

|---|---|---|

| Meeting prep still means reworking exports | Reporting flexibility; family office reporting | A strong family office platform should reduce cleanup and produce clearer views. |

| Principals want tailored views by entity or goal | Flexible outputs from family office software | The platform supports different cuts without one layout for every audience. |

| Investment decisions rely on one story across holdings | Data aggregation plus reporting continuity | Clean reporting matters when the full portfolio stays connected. |

Family office software earns its place when it helps the team communicate, not just calculate. The shortlist should favor tools that help family offices turn portfolio data into clearer reporting and better investment decisions.

Asset Managers Prioritizing Oversight, Permissions, and Scale

Oversight-heavy buyers care less about presentation polish and more about control. When asset managers serve multiple teams or client groups, the bigger question is whether the system can preserve portfolio oversight as operations expand.

| If this describes the firm | Weight these criteria most | Why it changes fit |

|---|---|---|

| User groups need different access | Security and permissioning | Asset owners, analysts, and operations staff should not all see or edit the same data. |

| The platform must grow with the business | Multi-entity handling; scale operations | A scalable system keeps governance intact as asset managers add demands. |

| Reviews span several teams or structures | Portfolio oversight; audit-friendly control | Financial institutions and hedge funds often need clearer accountability than presentation-first buyers. |

That shifts the shortlist toward platforms built for structured control. If scale, permissions, and oversight are the pressure points, the front end matters less than whether the platform keeps the model disciplined as complexity grows.

European Family Offices Balancing Service Model and Coverage

For European family offices, fit can depend on service-model alignment as much as feature depth. A stronger paper feature set may still be the weaker choice if support style or coverage does not match how the office works with private banks, trust companies, and outside advisors.

| If this describes the firm | Weight these criteria most | Why it changes fit |

|---|---|---|

| The office relies on high-touch outside relationships | Service-model alignment; coverage expectations | The right fit supports coordination with private banks and trust companies. |

| The team wants regional familiarity in support | Coverage and working style | european family offices may prefer a platform experience that matches local expectations. |

| Principals and service partners shape the decision | Reporting clarity plus service fit | A platform can look strong on paper and still feel awkward day to day. |

This is a fit question, not a geography score. When family offices need a platform that works inside an existing service network, coverage and support style can outweigh a longer feature list.

Complex Multi-Asset Teams Needing Stronger Consolidation

Consolidation becomes the deciding factor when portfolio complexity outruns reporting convenience. Teams handling private equity, private equity real estate, private markets, private investments, and other private assets need a system that can hold together complex structures without distorting the picture.

| If this describes the firm | Weight these criteria most | Why it changes fit |

|---|---|---|

| The portfolio spans public and private holdings across entities | Multi-entity and consolidation strength | multi asset portfolios are harder to read when entity and total views do not reconcile. |

| The team tracks direct investments and illiquid assets beside liquid exposure | Structural handling for private assets | A platform has to reflect timing, ownership, and valuation differences across multi asset holdings. |

| Reporting breaks down as structures layer up | Consolidation-heavy team priorities | The shortlist should favor platforms that stay usable as complex structures expand. |

Here, the shortlist shifts most sharply. When structural complexity becomes the real constraint, consolidation strength should carry more weight in the next comparison so the ranked shortlist matches how the firm operates.

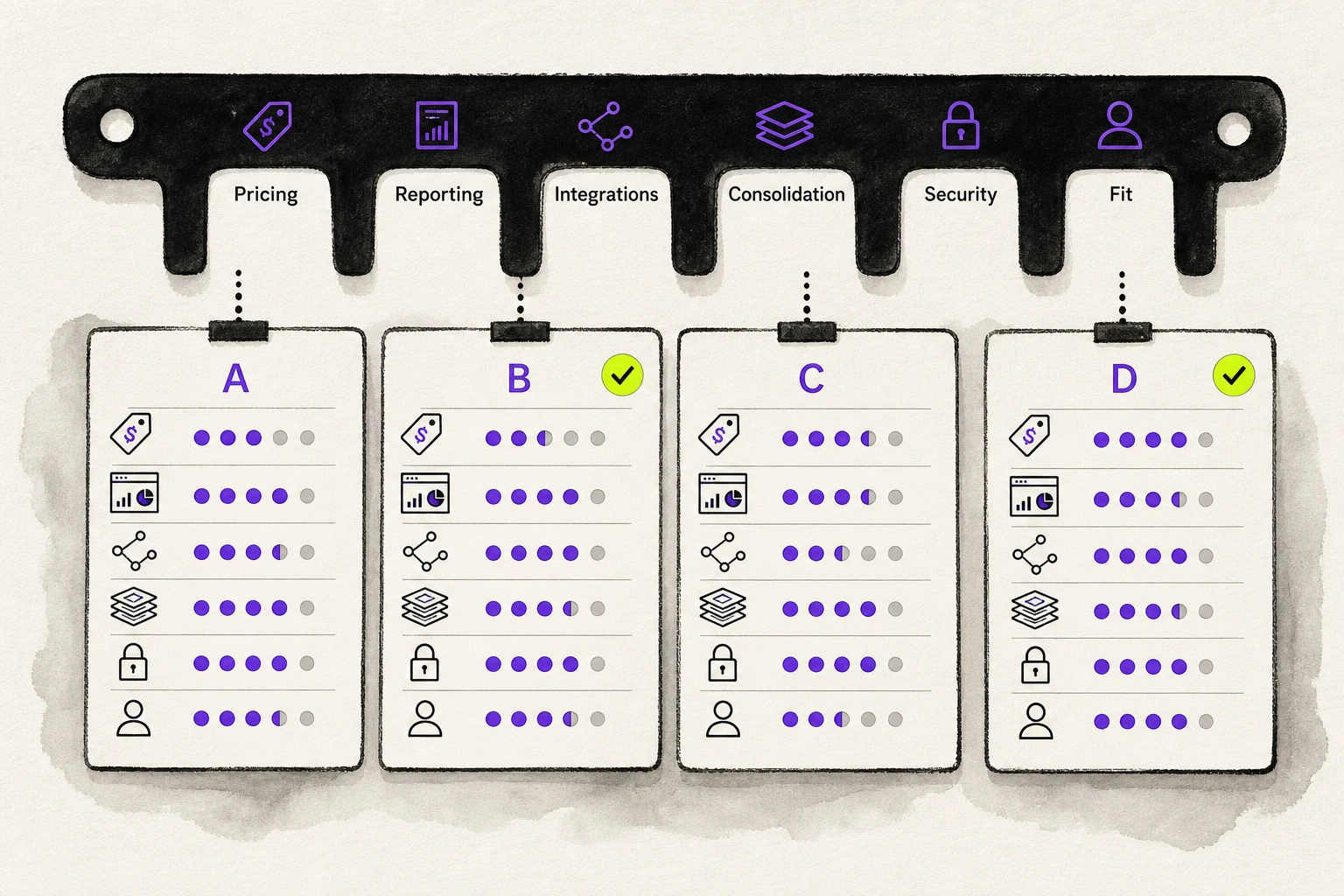

Top Alternatives to Landytech Ranked by Firm Fit

At this point, the decision is less about features in isolation and more about fit in practice. This view of the top alternatives to Landytech gives you one official shortlist reference, but it should be read as operating-context guidance, not as a universal best-to-worst verdict.

Each option was scored on the evidence for every criterion on a 1 to 5 scale, then combined into a weighted total, using criterion weighting: Accounting & general-ledger depth (0.25), Security & permissioning (0.12), Usability & onboarding (0.08), Reporting & dashboard flexibility (0.2), Data aggregation & custodian feeds (0.15), Multi-entity & consolidation (0.2). Weighting and scoring were computed from the cited sources, not estimated.

Benchmark (not ranked): Landytech is the incumbent reference point the ranked options below are compared against.

| Rank | Option | Weighted score |

|---|---|---|

| 1 | FundCount | 4.65 |

| 2 | Addepar | 4.63 |

| 3 | Asora | 3.53 |

| 4 | Dynamo | 3.44 |

| 5 | Copia Wealth Studios | 3.21 |

| Option | Accounting & general-ledger depth | Security & permissioning | Usability & onboarding | Reporting & dashboard flexibility | Data aggregation & custodian feeds | Multi-entity & consolidation |

|---|---|---|---|---|---|---|

| FundCount | 5 | No grounded evidence | 3 | 5 | 4 | 5 |

| Addepar | No grounded evidence | 5 | 4 | 5 | 5 | 4 |

| Asora | 2 | 4 | 5 | 4 | 5 | 3 |

| Dynamo | 3 | 4 | No grounded evidence | 4 | 3 | No grounded evidence |

| Copia Wealth Studios | No grounded evidence | 2 | 4 | 4 | 3 | 3 |

Sources:

- FundCount: FundCount.com – Hedge Fund Solution Sheet (PDF), FundCount.com – reporting, FundCount.com – general ledger, FundCount.com – family office software, FundCount.com – implementation

- Addepar: developers.Addepar.com – about Addepar, Addepar.com – family offices, Addepar.com – onboarding with Addepar the first 30 days

- Asora: Asora.com – family office accounting software, Asora.com – automated reporting in wealth management, Asora.com – sfo, Asora.com, Asora.com – security

- Dynamo: dynamosoftware.com – Dynamo Accounting Brochure NEW (PDF), dynamosoftware.com – our platform, dynamosoftware.com – Dynamo Integration Ecosystem Brochure (PDF), dynamosoftware.com – request rms3 0 demo

- Copia Wealth Studios: copiawealthstudios.com – reporting and performance, copiawealthstudios.com, copiawealthstudios.com – accounts, copiawealthstudios.com – security and data privacy, copiawealthstudios.com – self serve onboarding

Evidence coverage: 83% of the entity-by-criterion cells were backed by grounded evidence; cells without sufficient evidence were excluded from the weighted totals rather than guessed.

The table below shows which platforms rise when the buyer profile changes from reporting-led family offices to finance-led multi-entity teams or process-heavy alternatives-focused organizations. Use it to narrow the field, then read the qualitative profiles that follow to see where each option fits cleanly and where scope, controls, or rollout demands may change the buying decision.

Addepar

Addepar is a fit-oriented option for buyers that need broad aggregation, flexible reporting, and a way to pull complex entities and asset classes into one operating view. In plain terms, it suits mature teams that want a reporting-centered platform with deep data coverage and the governance to support a larger rollout, while the overall ranked order stays with the system-rendered table above.

Best Fit For

Addepar belongs on the shortlist when the buyer problem starts with fragmented data across custodians, entities, and alternatives rather than with ledger-first accounting needs alone.

- Complex family offices that need a single view across legal structures and portfolios.

- Wealth managers that need customizable reporting for different stakeholder groups.

- Teams with cross-custodian holdings and illiquid positions that are hard to assemble into one reporting layer.

Core Strengths

The strength of Addepar is its ability to connect aggregation, reporting, and controls inside one reporting platform. For firms that care about portfolio analysis and institutional grade analytics, that means fewer disconnected views when the portfolio spans multiple entities and hard-to-value holdings.

- Brings together multi-custodial data, illiquid alternatives, and complex legal entities in a single source-of-truth system.

- Supports interactive digital portals with granular permissioning for different users and audiences.

- Connects with hundreds of custodians, banks, and administrators for automated daily feeds.

- Documents granular role-based access control, audit logs, and SAML-based single sign-on.

Limits to Consider

Caution: Addepar looks better suited to teams that can support a more involved rollout. Official materials emphasize implementation services and a dedicated implementation team, and the available source set does not confirm a native double-entry general ledger or eliminations-based consolidation. Feed breadth is clearly extensive, but the published totals vary across official pages, so the safer reading is broad coverage rather than one exact figure.

Asora

Asora is easier to place when the buyer wants a family-office operating layer centered on reporting, aggregation, and day-to-day usability. The fit is strongest in private-wealth environments where wealth management teams value a clean experience as much as private wealth management visibility, and where a flagship platform does not need to be ledger-led from the start.

Best Fit For

Asora suits firms that want reporting and aggregation to sit close to the daily operating rhythm of family offices, especially when the experience needs to stay accessible for nontechnical users.

- Single family office teams that want one reporting-led operating layer

- Multi-family environments serving single family office clients with similar visibility needs

- Family offices that value a cleaner front-end experience more than confirmed native accounting depth

Core Strengths

Asora's appeal is that it packages aggregation, reporting, and usability into one family-office-oriented layer. For a team that wants cleaner data flow without rebuilding every process, the practical upside is faster access to organized information instead of scattered files and sesame data spread across separate tools.

- Positions itself as a family-office platform that centralizes data aggregation, portfolio management, and reporting.

- Supports integrations with thousands of financial institutions and uses Canoe for private asset tracking.

- Documents MFA, role-based permissions, ISO 27,001 certification, and detailed activity and audit-trail controls.

- States relatively fast go-live guidance in official materials, while keeping timing dependent on firm complexity.

Limits to Consider

Caution: the sourced story around Asora is strongest on reporting, aggregation, and usability, not on confirmed native accounting depth. Its own materials position it alongside a separate accounting or general-ledger stack; eliminations-based consolidation was not confirmed in the provided research, and official onboarding timing should be treated as vendor guidance that can vary by complexity.

FundCount

FundCount is the clearest fit when the shortlist needs an accounting-led option, not just a reporting-led replacement. It works best as an investment management platform for teams whose investment management process depends on the management platform staying close to the ledger, consolidation workflow, and control environment.

Best Fit For

FundCount belongs on the shortlist when finance and operations lead the buying process, and when reporting needs to stay tied to accounting records rather than sit in a separate layer.

- Finance-led family offices that need multicurrency accounting and stronger control over entity structure.

- Fund administrators and asset owners that need partnership accounting and consolidation support.

- Teams that want reports to come from the same underlying accounting record instead of from a separate presentation tool.

Core Strengths

FundCount's value in this shortlist is the depth the research confirms in the ledger and consolidation layer, not just in the presentation. For buyers that need finance controls, multi-entity visibility, and reports that stay linked to the underlying books, that creates a clearer operating picture instead of a separate reporting layer.

- Documents a real-time general ledger with double-entry, multicurrency accounting.

- Supports multi-entity, multicurrency, intercompany, consolidations, and partnership accounting.

- Explicitly references automatic elimination and intercompany eliminations during consolidation for family office use cases.

- Supports no-code or visual report design from the same general-ledger and partnership-accounting record.

- Describes automated custodian, bank, and pricing feeds, plus native connectors and broader app connectivity.

Limits to Consider

Caution: FundCount can read as heavier and more finance-oriented than a presentation-first buyer may need. The provided research does not confirm single sign-on on the retrieved official pages, and the migration example in the source set is a case example rather than a typical onboarding benchmark. That makes it a stronger fit for control-oriented teams than for buyers who mainly want a lighter reporting refresh.

Copia Wealth Studios

Copia Wealth Studios makes the most sense when the buying priority is stakeholder communication, polished reporting, and easier information capture around wealth structures. The fit is strongest for teams that want cleaner presentation and relationship visibility without assuming deep institutional accounting controls from the outset.

Best Fit For

Copia fits communication-led wealth environments where the platform needs to help family offices and wealth owners understand holdings, documents, and relationships more clearly.

- Family offices that want more polished stakeholder-facing reporting.

- Advisory teams serving wealth owners who need clearer visibility into entities and documents.

- Firms that value onboarding simplicity and relationship mapping alongside reporting.

Core Strengths

Copia's strongest case is around how information is gathered, structured, and presented back to stakeholders. In simpler terms, it helps teams turn scattered documents and account details into customizable reporting that is easier to share through a client portal and easier to review with mobile access when needed.

- Uses AI to ingest documents into structured data and update dashboards.

- Supports entity mapping and wealth relationship visualization for more intuitive context.

- Includes self-serve onboarding and connected-account or portal-linked workflows for data collection.

- Supports reporting metrics such as Net IRR, TWR, and TVPI, along with custom lenses for tailored views.

Limits to Consider

Caution: the available evidence supports Copia most strongly as a reporting and workflow platform, not as a deeply confirmed accounting control system. The provided research does not confirm a double-entry general ledger, eliminations-based consolidation, or published single sign-on support, and feed breadth is described more by workflow than by a published custodian-count benchmark.

Dynamo

Dynamo becomes relevant when the replacement decision reaches beyond reporting and into operational workflow. It is a better fit for firms where private equity, private equity firms, capital markets processes, investment management oversight, deal sourcing, and venture capital operations all shape the platform requirement.

Best Fit For

Dynamo fits organizations that need reporting inside a broader operational system, especially when investor workflows and alternatives operations matter as much as dashboards do.

- Process-heavy alternatives organizations with LP or GP workflows.

- Family office or investor teams that need onboarding, portal, and document processes in the same environment.

- Buyers who want reporting tied to a wider operational stack rather than to a reporting-first tool alone.

Core Strengths

Dynamo's appeal is breadth. Instead of stopping at reporting, the sourced material points to a platform that covers investor operations, workflow control, and fund-accounting support in one connected environment.

- Positions itself around alternative investments, with LP coverage that explicitly includes family offices.

- Supports investor onboarding, KYC and AML workflows, subscription documents, DocuSign, and investor-portal tasks.

- Describes fund accounting as general-ledger-based, with Excel-linked reporting refreshed from the general ledger.

- Provides an open API and integration framework, with documented connections to dozens of fund administrators and custodians.

- Supports configurable dashboards, workflows, and reports across a broader operating model.

Limits to Consider

Caution: Dynamo may be broader than necessary for a buyer who only wants a reporting-first replacement. The provided research does not confirm a double-entry ledger, legal-entity eliminations, or a published onboarding timeline, and the evidence on single sign-on and audit-trail controls is not presented consistently across the main site. That tradeoff matters most when the next step is a side-by-side decision on reporting depth, integrations, and firm fit.

How Top Alternatives to Landytech Compare for Reporting, Alternative Investments, and Firm Fit

Once the shortlist is clear, the decision stops being about finding one generic winner. It becomes a head-to-head trade-off across reporting flexibility, integrations context, pricing context, and alternative-investment fit. The system-rendered comparison earlier in the article is the anchor for that view. This section translates it into buying logic so strong options that look similar on paper start to separate in practice.

Reporting is usually the first dividing line. Some of the top alternatives to Landytech center more on presentation and client communication, while others tie reporting more tightly to accounting depth and entity-level controls. Addepar is often evaluated for flexible, polished output across portfolios. Asora fits buyers who want customizable reporting inside a family-office operating platform. FundCount ties reporting more directly to the same general-ledger record, which matters when reporting must stay close to reconciliation, consolidation, and audit-ready books. Copia Wealth Studios also leans into polished views, especially for firms that want portfolio visibility and document-driven communication in one experience.

Alternative investments create the next real split. Several platforms support private and illiquid holdings, but they do not frame that support the same way. Asora emphasizes commitments, capital calls, distributions, and valuations in a family-office workflow. Addepar focuses on alts data collection and extraction to improve visibility across asset classes. FundCount connects alternative investments more directly to accounting treatment, including statement ingestion and posting into the book, which can matter for finance teams managing complex asset allocation across entities. Dynamo differs in that the platform supports broader alternatives operations, including LP and GP workflows, investor processes, and portfolio monitoring.

Data breadth matters, but pricing context keeps the comparison honest. Asora and FundCount publish pricing structures publicly, while Addepar and Copia use sales-led pricing and Dynamo discloses its model without public rates. That does not mean the public pricing options are automatically the better fit. It means buyers should separate price visibility from total operating fit and read optional add-ons, implementation scope, or any hidden fees where vendors disclose them, rather than treating public pricing as a full cost picture. In plain terms, the cheaper-looking option can become the slower decision if it does not match the firm's reporting, integration, or controls needs.

Firm fit is where the shortlist usually narrows. A reporting-centric family office may prefer a faster path to dashboards, custom output, and broad aggregation. A finance-led organization with multi-entity complexity may value deeper books, partnership accounting, and cleaner consolidation. An alternatives-heavy team may need the platform supports operational workflows beyond reporting alone, including adjacent risk management tools or views that support wider oversight. Read the earlier system-rendered comparison table as a decision aid for those tradeoffs, not as a substitute for them. That is what turns shortlist confidence into a practical next step: knowing whether the real blocker is reporting, integrations, pricing context, or operating-model fit, and acting on that first.

What Asset Managers and Family Offices Should Do Next

A strong comparison only helps if it changes the next decision. For asset managers and family offices, the right next-step path depends less on abstract preference and more on what is failing now: reporting strain, structural complexity, or demo readiness.

The system-rendered comparison earlier in the article shows where the shortlisted platforms differ. What matters here is how to use that insight without forcing every team into the same buying motion. Some firms need a low-disruption reporting improvement; some need a complexity-driven evaluation; and some are ready to turn a shortlist into live validation questions.

If You Need Better Reporting Without Rebuilding Every Workflow

If reporting is the main problem, a full platform reset may be premature. Start by testing whether a low-disruption reporting improvement solves the real bottleneck.

- List the reports that regularly need rework or delay decisions.

- Ask each shortlisted vendor to show that exact workflow with a realistic output.

- Check whether the gain comes from presentation flexibility or cleaner data flow.

- Pause the search if stronger reporting fixes the pain without exposing bigger control gaps.

If Portfolio Complexity Is Already Outgrowing Your Current Stack

When the problem goes beyond presentation, convenience should stop leading the evaluation. Use a complexity-driven evaluation centered on consolidation and control.

- Map Where the Stack Breaks: reporting, aggregation, permissions, auditability, or consolidation.

- Use demos to test full operating scenarios, not isolated screens.

- Prioritize capabilities that reduce fragmented oversight across portfolios and entities.

- Treat ease of use as important, but not as the deciding factor when control is weak.

If You Need a Shortlist You Can Take Into Vendor Demos

Use demos to test fit, not restart discovery. Bring the article's firm-fit logic into due diligence with questions tied to real workflows.

- Ask to see your highest-stakes reporting workflow from raw inputs to final output.

- Request a live example using your entity structure, user permissions, and approvals.

- Test one difficult portfolio case where alternatives or consolidation create friction.

- Confirm what the team would need to change operationally after purchase.

- Ask which firm types get the most value and where fit is weaker.

Disclaimer

This article is for general informational purposes only and should not be considered legal, tax, financial, investment, accounting, or professional advice. Reading it does not create any advisor-client, consultant-client, or fiduciary relationship. Readers should consult qualified advisors before acting on this content. No liability is accepted for any loss arising from reliance on the information provided.

Information is believed accurate as of publication but may change over time, and some figures are drawn from third-party sources. Mentions of third-party firms, tools, reports, or institutions are illustrative and for context only, and do not constitute endorsement or criticism unless clearly stated.